Learning how to build an emergency fund isn’t just for people with extra cash. However, even if you’re living paycheck to paycheck, you can start one.

In fact, most people know they should have an emergency fund — but when money’s tight, it can feel impossible to start. Therefore, the good news is that anyone can build one that grows over time, even on a tight budget.

For example, a few smart habits and consistent small steps, you can protect yourself from surprises and build lasting peace of mind.

Ultimately, this guide will show you how to create your financial safety net from scratch, one intentional step at a time.

1. Start Small — and build your emergency fund Now

Don’t wait for the “perfect time” to save. Instead, start with what you can — $10, $20, even $5 a week. The power isn’t in the amount; it’s in the habit.

Next, start small by automating a transfer the day after each paycheck. You’ll train your brain (and your budget) to make saving non-negotiable.

💡 Pro Tip: Try a bank that lets you name your savings goal — like “Emergency Fund.” Seeing that label every time you transfer money reinforces your purpose.

2. Keep Your Emergency Fund Separate From Spending

However, if your emergency fund lives in your main checking account, it’s too easy to dip into it.

Open a separate high-yield savings account — ideally one that earns a little interest and takes a day or two to transfer money back out.

Open a high-yield savings account (see this essential guide to building an emergency fund) — ideally one that earns a little interest and takes a day or two to transfer money back out.

In addition, this extra “friction” makes impulse spending harder, while at the same time your money grows quietly in the background.

3. Cut One Small Expense (Not Your Entire Lifestyle)

You don’t need to cancel every comfort to save money. Instead, pick one thing — your daily coffee, unused subscription, or extra streaming plan — and redirect that small amount to your fund.

As a result, that $25–$50 a month adds up to $300–$600 a year — for example, enough to handle most car repairs or unexpected bills without reaching for a credit card.

4. Use Extra Money Strategically

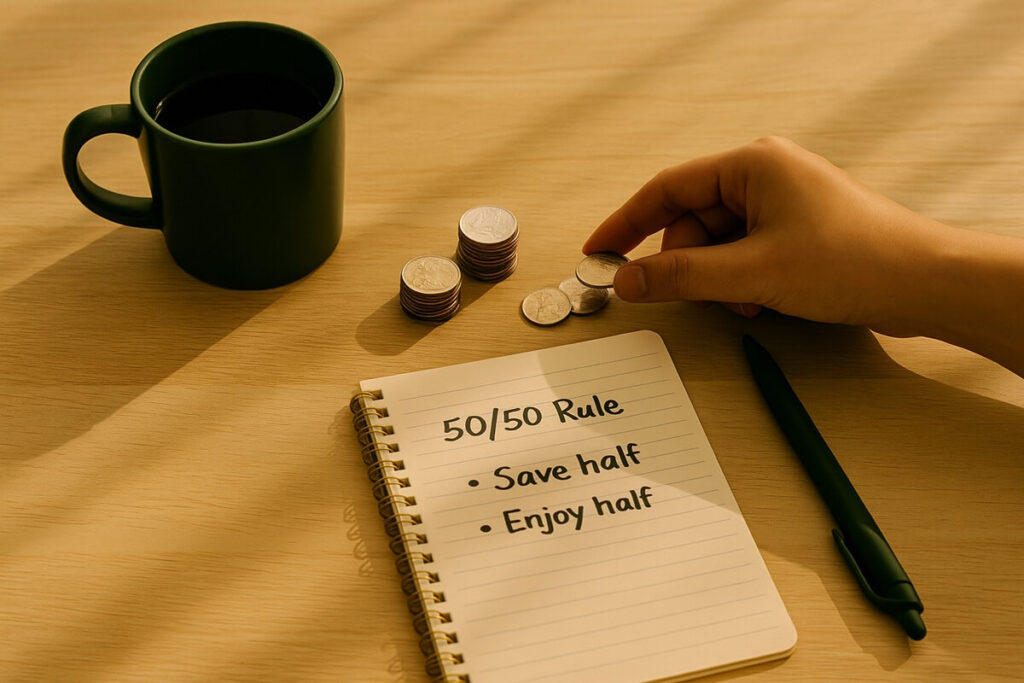

For instance, tax refunds and side-hustle income are golden opportunities. In other words, rather than spending it all, try a 50/50 rule — save half, enjoy half. You’ll still feel rewarded while building a real cushion for the future.

💰 Example: A $1,200 tax refund = $600 toward your emergency fund = one month’s rent or two car payments of security.

💡 Pro Tip: If you want to free up even more cash for your emergency fund, check out these simple money habits that help you save automatically without feeling deprived.

5. Define What Counts as an Emergency

Moreover, clarity prevents regret. An emergency fund is for needs, not wants.

True emergencies include:

- Job loss

- Medical expenses

- Car or home repairs

Not emergencies:

- Holiday gifts

- Vacations

- New tech gadgets

Consequently, define your personal rules now — before temptation hits — and you’ll protect your savings from slow leaks.

How Much Should You Save?

Aim first for $500–$1,000. That’s enough to cover most small emergencies.

After that, build toward 3–6 months of expenses.

If your job is unstable or self-employed, lean closer to six. Otherwise, if your income is steady, three months may be plenty.

🎯 Quick Math: Monthly expenses × 3 = your starter goal

(Example: $2,000 × 3 = $6,000 emergency fund target)

For example, for a quick breakdown of insured banks and limits, see the FDIC deposit insurance guide.

Final Thoughts

Overall, building an emergency fund isn’t about perfection — it’s about momentum. Every dollar you save buys you peace of mind, confidence, and control over your life.

So, start small, stay consistent, and celebrate your progress.

Frequently Asked Questions

How much should I keep in my emergency fund?

Aim for $500–$1,000 to start, then grow it to 3-6 months of essential expenses. Over time, adjust your target as your life or income changes.

Where should I keep my emergency fund?

Keep it in a high-yield savings account separate from your checking. That keeps it accessible but out of sight, so you’re less tempted to spend it.

Building financial freedom starts small — like setting aside your first few dollars for emergencies.

Each small win compounds over time. Keep making those consistent choices, and you’ll build both confidence and security along the way.

At Earned Future, we believe lasting freedom isn’t found — it’s built.