The phrase emergency fund vs sinking funds can sound like one of those money topics that makes things more complicated than they need to be. At first, both seem like savings. Both involve setting money aside. Both should help you avoid financial stress. So it is easy to look at the two and think, “Does it really matter what I call it?”

The difference matters more than it seems.

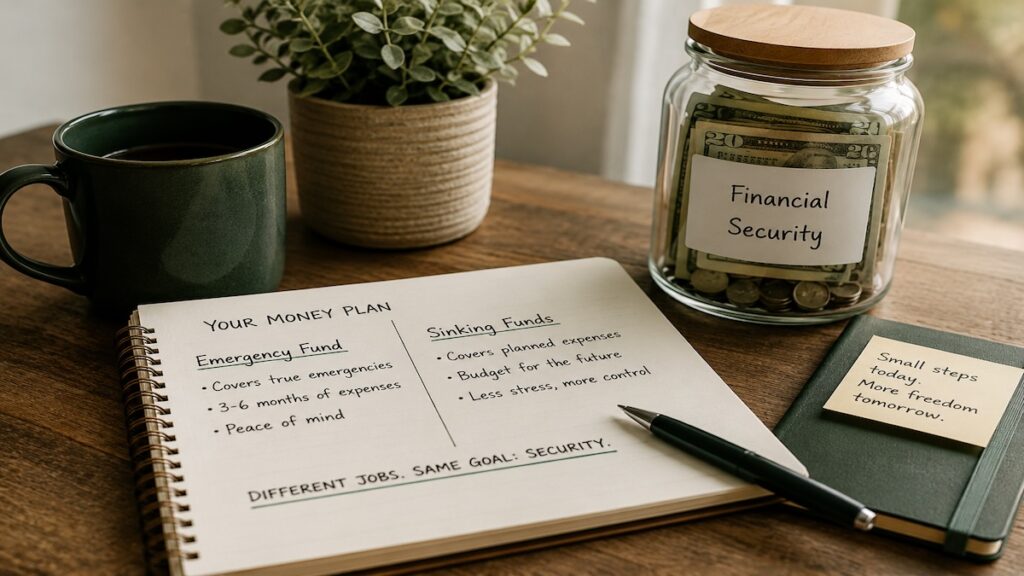

An emergency fund protects you when life disrupts your normal plan. Sinking funds help you prepare for costs you already know are coming. One protects against the unexpected. The other gives predictable expenses a place to land before they turn into pressure.

That does not mean you need a separate savings account for every little thing. Some people like that style because it helps them see the money clearly. Others prefer one main high-yield savings account, one cash pile, or a simple note that reminds them what future costs are waiting in the background.

The structure can stay simple. The real issue is not the number of accounts. It is the job you expect the money to do.

Why Emergency Fund vs Sinking Funds Matters

This is where many people get stuck. They build an emergency fund, feel good about finally having savings, and then life starts using that money for things that were not really emergencies.

Tires. Insurance renewals. Christmas. Car registration. Home maintenance. A yearly bill that somehow arrives faster than expected.

None of those costs mean you did something wrong. Most are normal parts of life. The problem starts when every irregular expense comes from the same money that should protect you from true disruption.

That is how savings can feel like it keeps disappearing, even when you are trying to be careful. You are not always failing to save. Sometimes you are asking one pool of money to handle too many different jobs.

Understanding the emergency fund vs sinking funds difference helps clear that up. Labels do not magically fix your money, but clear roles make better decisions easier.

What Each One Is Actually For

An emergency fund handles disruption. Think job loss, sudden medical costs, urgent repairs, or a major issue you could not reasonably plan around. The point is stability. Emergency money helps you keep life from falling apart when something unexpected hits.

A sinking fund handles expected expenses. Think car tires, annual insurance, holidays, property taxes, routine maintenance, school costs, or a large purchase you know will probably happen. The point is preparation. This money gives normal future expenses room before they become urgent.

That difference can sound small until you watch what happens in real life.

Say your car needs tires. If the tires wore down over time and you knew the replacement was coming, that cost does not belong in the same category as a sudden job loss. It may still feel stressful. It may still be expensive. But the expense followed a pattern you could see.

Now compare that with your furnace breaking unexpectedly in the middle of winter. That kind of situation interrupts your life in a different way. You did not choose the timing, and you may not have had a clear warning.

That is the kind of disruption an emergency fund exists to soften.

Why Using One Fund for Everything Creates Stress

When these two types of expenses share the same money, confusion builds fast. You use emergency savings for predictable costs, then feel behind when a true emergency happens. Or you avoid touching savings altogether because you are not sure what the money is really for.

Clear roles remove some of that tension.

A sinking fund does not have to be fancy. It does not have to live in its own account. At its core, it simply means you recognize that some expenses are already on the way, and you stop pretending they belong in the same category as emergencies.

That shift protects your emergency fund from doing every job at once. It also helps you see predictable expenses more honestly. Instead of treating tires, holidays, taxes, and annual bills like surprises, you start seeing them as normal costs that need space.

The goal is not to make your money system more complicated. The goal is to stop letting every larger expense feel like the same kind of problem.

The Emergency Fund vs Sinking Funds Difference in Real Life

The easiest way to test the difference is to ask one question: could I reasonably see this coming?

If the answer is no, you are probably looking at emergency fund territory. A sudden job loss, urgent medical bill, or unexpected major repair can shake your stability without warning. That is why emergency money needs to stay protected. It gives you options when life does something you could not plan around.

If the answer is yes, the expense probably belongs closer to a sinking fund. That does not mean you knew the exact date or the exact amount. It only means the expense followed a normal pattern. Cars need maintenance. Homes need repairs. Holidays return. Insurance renews. Kids grow. Appliances age.

That difference matters because expected costs feel less chaotic when you stop treating them like random events.

This also connects to the bigger idea from Why Predictable Expenses Still Feel Like Emergencies. Many expenses feel urgent not because they were truly surprising, but because they did not have enough room before they arrived.

What Belongs in Each Category

You do not need a perfect rulebook to separate the two. You just need enough clarity to avoid draining the wrong money.

Emergency fund money should protect your stability. It is for the kind of disruption that could throw your life off course if you had no backup. Job loss, a sudden medical situation, urgent travel, or a repair that truly could not wait all fit that purpose.

Sinking fund money is for expected pressure. It helps with the costs that do not happen every month but still belong to normal life. Vehicle maintenance, property taxes, annual subscriptions, holidays, school expenses, home projects, and insurance premiums all fit here.

Some expenses can sit in the gray area. A car repair might feel like an emergency if it happens suddenly. But if the brakes have been getting worse for months, that cost was probably moving toward you for a while.

The point is not to judge every expense perfectly. The point is to notice the difference before everything pulls from the same place.

Emergency Fund vs Sinking Funds Is About Jobs, Not Accounts

This is the part that gets overcomplicated. People hear “sinking funds” and picture ten separate accounts, each with its own label, transfer, and rule. That setup works for some people, but it is not required.

A sinking fund can live inside one savings account if you track it clearly. It can be a line in a spreadsheet, a note in your budget, a rough mental number, or a portion of your high-yield savings account that you know is not truly available for everyday spending.

The job matters more than the container.

If you prefer fewer accounts, that is fine. A simple system you actually use will beat a detailed system you abandon. The only danger is letting one big savings balance look more available than it really is.

For example, a $10,000 savings balance may feel strong. But if $2,000 will likely go toward tires, insurance, and home maintenance soon, then the whole $10,000 does not have the same job. Some protects you from emergencies. Some waits for expected costs.

Seeing that difference helps your savings feel more honest.

Why This Protects Your Emergency Fund

When predictable costs keep pulling from emergency money, your emergency fund never gets to fully do its job. It turns into a catch-all account for anything larger than usual.

That creates a frustrating cycle. You build savings, use it for something expected, then feel like you have to start over. The balance may recover eventually, but the trust in the system gets weaker each time.

A clearer separation helps stop that cycle. Not because the money becomes untouchable, but because you understand what each part is there to protect.

Your emergency fund protects stability. Your sinking funds protect cash flow. One keeps life from falling apart. The other keeps normal expenses from feeling like a crisis.

That is the simple difference most people miss.

A Calm Close

Emergency fund vs sinking funds is not about making money more complicated. It is about giving your savings clearer jobs.

An emergency fund is for the costs you could not reasonably see coming. Sinking funds are for the costs you can see coming, even if the exact timing or amount is not perfect. One protects you from disruption. The other helps normal life stop feeling so disruptive.

You do not need a dozen separate savings accounts to make that work. You just need enough awareness to know when money is protecting you from the unexpected and when it is waiting for something predictable.

Once that difference becomes clear, savings starts to feel less confusing. You stop wondering why your emergency fund keeps disappearing, and you start seeing which expenses needed their own place in the plan all along.

Once you understand that these two types of savings solve different problems, the next question becomes much simpler: what should a sinking fund actually be doing?

That is where the next part of the system begins.